Chapter 3 – Environmental

The E in ESG: Environment

The “E”/Environment in ESG considers how a company performs as a steward of the natural or physical environment. It takes into account a company’s utilization of natural resources and the effect of its operations on the environment, both in its direct operations and across its supply chains.

It is important that companies consider a wide variety of topics regarding their environmental impact when conducting a materiality assessment:

- Water use, treatment and discharge;

- Soil health and management;

- Noise pollution affecting all living animals and humans; and

- Air quality includes the impact of greenhouse gas emissions — leading to Climate Change, but also other emissions that may have unique air quality impact.

- Resource: for auto shredders, ReMA has put together guidance on VOC Emissions

Biodiversity, or the variety of life in the world or in a particular habitat or ecosystem, is impacted by all of these and is increasingly a focus of a broad range of stakeholders, including investors, regulators, employees, and customers.

Although each of these categories warrants its own discussion and they are all interconnected, this toolkit focuses on air quality, and more specifically Greenhouse (GHG) emissions. Our main sources are the globally accepted Greenhouse Gas Protocol’s Corporate Standard (GHG Protocol) and US EPA’s Center for Corporate Climate Leadership. For more information on these topics, as well as the link to material issues for the recycled materials industry, please refer to Workshops #1 (Materiality), #3 (Environment is more than Emissions), and #7 (Biodiversity).

What are Greenhouse Gases?

Greenhouse gases are the six gases that trap heat in the atmosphere, including: carbon dioxide (CO2); methane (CH4); nitrous oxide (N2O); hydrofluorocarbons (HFCs); perfluorocarbons (PFCs); and sulphur hexafluoride (SF6).

There are other types of air emissions that are not considered GHG because they do not react to trap heat in the atmosphere such as: nitrogen, oxygen, argon, neon, hydrogen, and carbon monoxide.

Why focus on reducing GHG emissions?

As the impacts of climate change caused by GHG emissions become increasingly well-documented, many governments, national and state/provincial, are taking steps to reduce GHG emissions through policy. As a result, companies need to understand their own GHG risks in order to stay competitive, and to be prepared for future regulations.

Taking inventory of GHG emissions can serve several purposes:

- Knowing your emissions helps manage GHG risks and identify reduction opportunities;

- Public reporting and participation in voluntary GHG programs may position a company well for both required and voluntary reporting;

- A GHG inventory facilitates participating in cap and trade, or carbon trading programs that can be financially beneficial, or even required; and

- Early voluntary action may help support “baseline protection” and /or credit for early action.

Conversely, companies with a limited focus on company’s direct emissions may result in missed GHG risks and opportunities, which may lead to a misinterpretation of the company’s actual GHG exposure.

What gets measured gets managed. The process of accounting for your emissions can help identify the most effective reduction opportunities – which can drive efficiency and even the development of new products and services that can help differentiate the company or its suppliers.

Emissions Categories

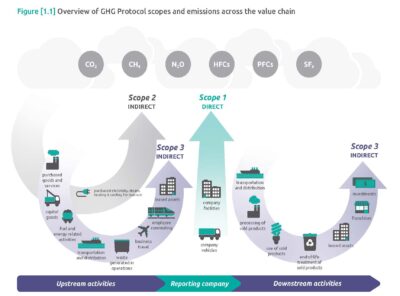

The GHG Protocol establishes 3 different types of GHG emissions:

- Scope 1 emissions are all direct emissions from the operations of the company. If you look at the green arrow in the middle of the graphic below, you can see that Scope 1 emissions cover the activities directly controlled by the company, such as fuel combustion in their equipment and vehicles.

- Scope 2 emissions, in grey on the left, are indirect emissions and are specifically from electricity purchased and used by a company.

- Scope 3 are other indirect emissions that are part of a company’s supply chain (blue arrows on either side) but are from sources that they do not own or control. They may be associated with procurement, transportation and distribution performed by 3rd party vendors, from product use, or end-of-life emissions. These are often referred to as Supply Chain or Value Chain emissions and they may be the majority of the emissions for some industries. There is increasing focus on quantifying these emissions.

Source: GHG Protocol

The purpose of these scopes is to avoid double counting emissions.

Spotlight on Scope 3:

Many companies report only Scope 1 and 2 emissions today, but Scope 3 emissions are increasingly being asked for by customers and regulators. Scope 3 emissions can be divided into 2 main groups: upstream and downstream emissions. Upstream emissions include all emissions associated with the production of goods and services, while downstream emissions include any emissions produced during their use and disposal.

Upstream activities include:

- Purchased goods & services

- Capital goods

- Fuels-and-energy- related activities (not included in scope 1 or scope 2)

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

Downstream activities include:

- Transportation and distribution of sold goods

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets

- Franchises

- Investments

Reporting Scope 3 emissions creates a complete assessment of a company’s impact across its value chain. Recycled materials companies tend to produce a lower percentage of Scope 3 emissions. However, in the retail industry, approximately 98% of emissions are from Scope 3 categories.

Understanding Scope 3 emissions enables companies to target reduction strategies for maximum impact. For companies with a high percentage of Scope 1 emissions, such as those from fleets or equipment, efforts can focus on reducing fuel consumption. In contrast, companies with significant Scope 3 emissions must navigate more complex relationships with suppliers and customers to drive emissions reductions across the broader supply chain. Every company is part of someone else’s supply chain.

Please refer to Workshops #3 (download slide deck) and #5 (download slide deck), and our June 2025 Webinar on Supply Chain Transparency (download slide deck) for more information on Scope 3. Please note that Workshop 3 was recorded prior to the 2023 California climate disclosure legislation and both workshops were recorded prior to the 2024 SEC climate disclosure rules, which were subsequently put on hold in spring 2025.

Avoided Emissions

In addition to Scopes 1, 2 and 3 emissions, Avoided Emissions are a topic of interest in the recycling industry in particular. Avoided emissions are exactly what the words say – emissions that didn’t get generated. These are sometimes referred to as “Scope 4” emissions, although they are not an officially recognized scope by the GHG Protocol. The GHG Protocol established the methodology for measuring emissions, but it doesn’t establish protocols for measuring avoided emissions, since the total inventory will capture reductions.

To avoid double counting of emissions, companies are expected to ONLY report their direct and indirect emissions from their company’s operations such as fuel use or electricity used in their recycling operations. Claims of avoided emissions associated with recycling are reported separately from scopes 1, 2, and scope 3 emissions.

Recyclers often use EPA’s WARM tool (Waste Reduction Model (WARM) | US EPA) to calculate the benefits of the tons they manage for recycling. They may use statements like “our company’s recycling saved the equivalent of planting 100 trees each year.” It is absolutely fine to do this! A lot of companies do this kind of storytelling to bring attention to the value of the services that they provide. Although they don’t get the actual emissions reductions credit for it in their own GHG inventory, their company plays an important role in facilitating the environmental benefits of recycling.

Avoided emissions data is valuable information to provide to a company’s stakeholders, but it is separate from a company’s GHG emissions inventory. Here is a summary of the different ways that you as a recycler might be avoiding or reducing emissions in other parts of the supply chain:

Refer to Workshops #3 (download slide deck) for an introduction and #5 (download slide deck) for more details about Avoided Emissions, and to US EPA’s Center for Corporate Climate Leadership (EPA Center for Corporate Climate Leadership | US EPA).

Refer to Workshops #3 (download slide deck) for an introduction and #5 (download slide deck) for more details about Avoided Emissions, and to US EPA’s Center for Corporate Climate Leadership (EPA Center for Corporate Climate Leadership | US EPA).

GHG Inventory

The Paris Climate Accord requires a reduction of emissions sufficient to keep global warming below 1.5 degree Celsius. Measuring emissions plays a key role in that effort. There are four key steps to tracking emissions:

- Reviewing accounting standards and methods. Determine your organizational boundaries and operational boundaries and choose a base year for your emissions. The base year should be the first year that you use to track your emissions changes.

- Collect data and quantify GHG emissions.

- Document everything and develop procedures. This will help with audits and in future years when questions arise.

- Enlist a 3rd party verifier to audit and verify data, and the process itself.

Carbon Credits, Offsets and Insets

Carbon credits and offsets are accounting mechanisms representing compensation for the reduction or removal of GHG emitted somewhere else. Both represent the reduction or removal of one ton of carbon dioxide or its equivalent in other greenhouse gases. Carbon insetting is a newer concept that involves investing directly in carbon reduction within your supply chain. The following are some key differences between them:

- A carbon offset is the removal of GHG from the atmosphere (carbon sequestration) outside a company’s own value chain while a carbon inset removes GHG from within a value chain. They are often considered voluntary.

- Carbon credits are a reduction in GHG released into the atmosphere. They are often required by government policy (e.g., Cap-and-Trade programs).

A rule of thumb is to create a goal to reduce your absolute emissions as much as possible, before tapping into carbon markets.

Resource: Offsetting vs. Insetting Jargon Buster from Climate Action for Associations

Calculating GHG Emissions

Many companies can get started on emissions calculations using US EPA’s Simplified GHG Emissions Calculator. The Calculator is designed as a simplified calculation tool to help small business and low emitter organizations estimate and inventory their annual greenhouse gas (GHG) emissions. The calculator will determine the direct and indirect emissions from all sources at an organization when activity data are entered into the various sections of the workbook for one annual period. The Simplified GHG Emissions Calculator is supported by Excel 2021 or later (PC and Mac). It is free to use and was updated in 2023. It is generally updated on an annual basis. The Environmental Data Gathering Template, developed for this toolkit, can assist you in preparing to use this calculator.

GHG emissions in the recycling industry typically occur from the following categories:

- Fuel used in equipment in your facilities.

- Fuels in transportation vehicles such as cars and trucks.

- Emission from industrial processes associate with cement manufacturing, petrochemical processing, aluminum smelting, and other industrial processes.

- Emissions from equipment leaks, as well as fugitive emissions from landfills and gas processing facilities and other sources.

- Electricity that is purchased for a company’s operations.

Depending on the size and services provided by your company, there may only be a few key areas to focus on for your emissions inventory, facilitating the process of calculating GHG emissions.

Our ESG Workshop from August 2023 (download slide deck) provides more details about using the calculator.

Our How-To Guide explains the specific purpose and use case for all the calculators mentioned here.

Practical Tips & Technology

For practical tips on how to make progress in emissions reductions, check out ReMa’s February and May 2024 webinars, which features insights on technology to support ESG in the recycled materials industry, and ReMA members sharing the ways they have reduced emissions in their own operations.

ReMA’s August 2025 Webinar on Value Creation also featured member sharing how their waste reduction program created value for the company.

Resource: Download member case studies on energy efficiency and waste reduction impacts.

Summary

Many companies are already required to report on their GHG emissions, and a growing number of companies are being asked by their customers to provide this information for their reporting purposes. Getting ahead of this trend allows for risk mitigation and even value creation in terms of service offerings to customer.

Note: Please refer to relevant sections of ESG Workshops #2 (ESG Goal-Setting) and #3 (Tracking Emissions) for an overview of GHG emission reduction goal-setting.